A step-by-step guide to how Google demolished publisher ads

A step-by-step guide to how Google demolished publisher ads

The deadliest predators run silent and run deep, but every now again, they pop above the surface and into the light of day...

Welcome to new subs overnight from Reuters, the New York Times, SXSW, Accenture, IBM, Taboola, News Australia, Australia’s Nine, news.com.au, the Change Africa Initiative, the Sydney Morning Herald, the Australian, Optus, MyLondon, Finland’s Lähimedia Oy, and WeTransfer out of London, among others.

Ripper to have you along.

And thanks to my sponsor for making the magic happen. Cheers 👋

Also, after a couple of requests, I’ve also begun syndicating my column. If you’re interested in running it on your site, message me through Substack.

Let’s go…

Australia where I live is famous for sharks. Big, nasty, bitey, white ones. We have killer spiders too, and snakes, but it turns out, none of them were as vicious as our bankers.

Bear with me, this is about publishing, but I need to set the stage for what’s to come.

Not very long ago, every Australian was being beaten up by the banks. Fees were out of control, and the wealth gap was horrendous, and getting worse.

Authorities were turning a blind eye until eventually, and despite political opposition, a Royal Commission was launched.

Over months, it systematically exposed predatory lending, the exploitation of vulnerable customers, and even dead people being charged for non-existent products.

We learned that for years, banks prioritised profits over customers and that the financial institutions tasked with regulating them were weak and lenient.

So far, $3.15 billion has been refunded to people who were mis-sold and bullied, $2 billion has been levied in fines, and tainted CEOs, execs and board members have been punted or quit under a cloud.

Thousands of middle managers went as dodgy insurance and superannuation schemes were shelved, and the fat and lazy regulators were overhauled.

It became a catalyst for a commercial and cultural shift. Banks now emphasise customer outcomes, governance, and risk management. Imagine that…

Commission chief Kenneth Hayne said: “Pursuit of profit, and short-term profit at that, has trumped consideration of how the profit is made.”

We saw sense win over dollars for a change.

“We’ve a long way to go,” one confessed. “There’s a lot we need to fix.” “The industry has a lot to do to restore trust and confidence,” another admitted.

I’m focused on this because two things were clearly true then, and clearly true about Google now.

We all know something’s wrong because we all feel it in our hip pockets, and

The perpetrators won’t stop unless their dark acts are exposed to the light.

I’m going to do that today (and if you have anything breakable within arm’s reach, you might want to move it).

The past year has seen thousands of Google’s internal mails dragged out into the open.

We haven’t seen a smoking gun because Google many more, but what we have seen paints a different image of the Big Friendly Giant that Google wants the world to see.

We’ve all seen the Googlers. Sometimes it’s the CEO on stage; gangly, friendly, geeky. Pivot host Scott Galloway calls Sundar Pichai a $237 billion heatshield. Love that.

We see their execs doing their thang, with a pristine slide decks and selling their snake oil.

It all feels so damn plausible, only the ad antitrust trial underway now - just like the Royal Commission above - is dragging what they say and do out of sight into the public arena to be judged.

I’m about to share a jaw-dropping mail.

It was written at the dawn of Google’s drive to pool publisher ad inventory to sell it programmatically. It was step one of publishing being led to the gallows.

The mail is by the architect himself, and he reveals in painstaking detail what he wanted to do, how he’d do it, how to crush rivals, and disintermediate publishing.

His is a one-sided ad-centric vision for the future of publishing that has since left half of the world a news desert, and more than half the world’s journalists out of a job.

Google is continuing its defence this week, but yesterday’s evidence was boring and technical. Reporters in the court created a crossword to stay entertained.

So take the moment to read into this, so you can see the Google guys with the clarity that Australians now see bankers - with the blinkers off.

Is your hip pocket hurting? Is Google’s $238 billion in ad revenue rankling you? Do you feel you’re being taken advantage of? Would you trust it with your mortgage?

I thought not. And you’re right, because this is what they really think…

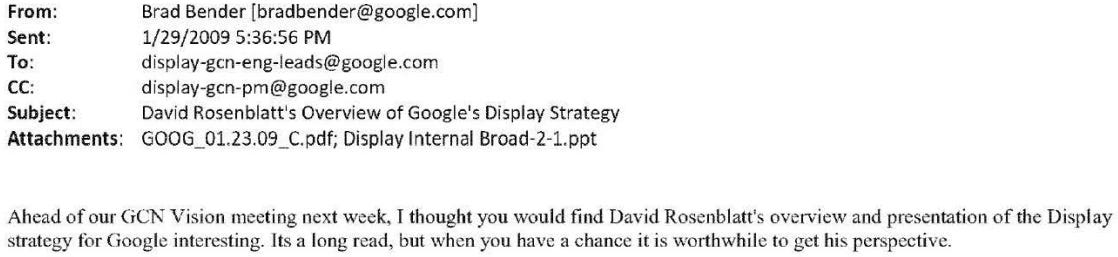

January 29, 2009. Obama had just become President, and Sully ditched a passenger jet in the Hudson. A few months earlier, Google spent $3.1 billion buying DoubleClick.

The goal was to start selling other people’s ads - publishers’ ads mainly, and over at the Googleplex, the company was beginning to reveal its plans to its global exec team.

It prompts Brad Bender, then Google’s VP of video and ad products, to send an email to his teams around the world...

Rosenblatt came to Google with the DoubleClick acquisition, and had been promoted to President of Ads, tasked with building the largest ad empire in history.

This is what he said:

“For years, DoubleClick toiled away in its corner, focused on the plumbing and advertising technology that everyone used, but most people don’t really think about.

“Eventually, we became almost ubiquitous, delivering 15 billion display ads a day. We touched almost every display ad in some form on the internet.

“We decided to look for a media partner and ended up being bought by Google.

“Right after, something like $12 billion of M&A (mergers and acquisitions) took place.

“Overnight, the sector went from a not-really-thought-about backwater, dominated by small, independent vendors to one run by a few big companies.

“So, what happened and what are the implications?”

He begins by focusing on inefficiencies at publishers and advertisers.

“Let’s start with publishers.

“In the network business, you have to understand that while the advertisers account for the revenue, the business depends on relationships with publishers.”

I have consistently said since the beginning, that Google won because of publishers.

He confirms it:

“If you don’t have access to inventory, you have nothing to say to advertisers. Now, put yourself in the position of a publisher.

“If you’re a publisher, this is how you think about your business. There’s always some small per cent(age) of unit volume that the publisher sells directly.

“It’s good inventory with high brand value. Expensive to make and to sell. You have to buy tech specific to sell the inventory, have the three martini lunches with agencies...

“Then you have this other stuff called remnant inventory that you just don’t know what to do with.

“(Publishers) hire someone who will call up a couple of ad networks. They’ll make a couple of deals, let them compete, and that’s it. That’s how they ran their business.

“The problem is that it’s inherently suboptimal. There are hundreds of networks. Maybe none of the networks you work with can give you the most for a given piece of inventory.

“It’s too hard to do 100 deals. It’s not worth the time to manage individual contracts, relationships… so, you end up exposing your inventory to a very small part of the market.

“You’re (also) making this inventory allocation decision without knowing where the demand is. Your homepage is premium (but) my stock quotes is remnant.

“But maybe there’s someone in the market willing to pay 10x more for the stock quotes page than the networks can get you.

So, you’re limiting the universe of who can sell your inventory (to)… You’re almost guaranteeing you’ll leave a lot of money on the table.”

Squirming yet? I was as I lived through it, but it’s about to get worse.

Rosenblatt continues:

“From an advertiser POV, the market is similarly inefficient. It’s too complicated, too expensive to execute ad buys.

“With third party ad serving, we think of it as just that, there’s a third party - and that’s it.

“If you map out an ad transaction, you could have seven or eight vendors, each with their own server, accounting methodology, (and) billing practices.

“…all in an industry where there are hundreds of thousands of publishers.

“So, the industry has all the characteristics of one that’s inefficient, immature, and isn’t working to its potential. That’s the industry landscape.”

It’s hard to disagree.

Rosenblatt now begins to share Google’s vision to disintermediate publishing.

“Let me walk through, from a publisher point of view, what fixes this.

“An individual publisher buys technology from DoubleClick and uses it for serving premium inventory.

“But it’s too expensive because the serving fees for DoubleClick are too large (compared to) what the networks give them for remnant.

“How to solve this… You have tech that looks across every piece of sellable inventory and introduces a layer so every network can compete for inventory.

“Instead of applying your DoubleClick ad server to your premium stuff only, you run all of your inventory through it.

“And instead of doing the deals with networks, you just say, go to www.adexchange.com, and bid for inventory there.”

Let’s break that down.

The ad networks were built for selling low-yield high-volume remnant ads.

Google now wants publishers to bundle premium ads in there too.

Google wants to because it needs vast volumes of premium ad inventory, and

Publishers said yes to get access to more buyers, which Google also controlled.

The outcome was Google had a multi-sided marketplace controlling supply, demand, auction, analytics, and pricing.

Rosenblatt clarified so no-one missed the point:

“If you win the auction, you get (the ad), and if you don’t, you don’t. Now you’re working on one platform, you can expose all of your premium inventory to the networks.

“Instead of three networks competing, you have hundreds. The end result is you guarantee yourself the highest yield for each impression.

“And in addition, your costs are lower, since you can reduce the size of your direct sales force. They can focus on selling only the most premium.”

Multiple times, Rosenblatt alludes to helping publishers, and it kinda comes across as genuine. Many trends he identifies are real. I recognise them.

But he also makes some bad assumptions that publishers accepted as gospel.

The biggest leap was that CPMs would stay high after publishers shoved their premium ads into Google’s ad network mangle.

This is what actually happened…

Google has a 91 per cent share of the global ad server market.

Google banked US$238 last year - 87.5 per cent of it came from ads.

Its auction tool Google Ads controls 87 per cent of global ad demand.

Its ad exchange AdX trades 56 per cent of the world’s ads.

It delivers 13 billion ads a day to publishers worldwide.

Nine in 10 global publishers rely on it.

So do eight in 10 of the world’s advertisers.

Two fifths of global video ads are traded there.

Google Ads locks ~83 per cent of Google Ads into its own auctions.

Publishers who want the ads have no option but to use Google ad tech.

Four in five of News Corp’s ad dollars come through GAM.

Three in five of Daily Mail’s ads come from Google.

The DoJ alleges this “tying” makes Google unavoidable.

The Daily Mail gave up leaving Google as it would cost US$4 million-a-year.

News Corp dropped the same plan because it would lose $9 million a year.

Lost ad revenue led to job losses and cuts at News Corp and Daily Mail.

USA Today’s publisher said collapsing ads forced it to fire 22,000 employees.

Google’s prices are “sky high” because it needs to keep growing.

It charges a 36 per cent levy on every ad traded through its tech.

These fees are double those of its rivals, and they are unregulated.

They are 10x the fees charged by credit cards, which are regulated.

It now banks the global earnings of all global publishers every three days.

Rosenblatt then shares his secret for growing at the same rate as the internet. Back in 2009, Yahoo and Microsoft were the biggest rivals. He said:

“Yahoo towards the end of 2006 reached a basic conclusion that applies to all internet publications.

“If you look at traditional media, the way they think about their business is very simple. It’s only in terms of their audience.

“If you run CBS, the only thing that matters is making sure your share of total audience - ratings - grows at a rate equal or greater than the overall market.

“Your share of the market translates into your share of ad revenues. If you grow share, you get promoted; if you lose you get fired. It works like this for TV and print.

“Yahoo applied this to their own business for years, but the conclusion they reached, which I think is right, is that it’s flawed for the internet.

“The cost of entry for a new publisher is so low, (traditional mass media) will never be able to grow their audience at the same rate as the internet.

“Some 21-year-old kid makes a website and gets huge share. Look at Facebook. The audience gets diluted.”

I remember this narrative. I spent hours gathering and sharing data with advertisers and agencies to explain the value of our audience.

Visit frequency, time spent, high click throughs - all were many times higher than platforms, but Google had convinced agencies and advertisers not to care.

Google’s business model was scale at any price. That needed:

Publishers to hand over their audiences (big tick) and advertisers to place ads with cheap networks on Google tech (tick two).

The outcome was less revenue for publishers = less publishers = less premium inventory = less options for agencies = less revenue for agencies = more need for Google’s cheap automation.

Rosenblatt spells it out:

“How do you fix this problem and grow your revenues at the same rate as the internet? It’s simple: By selling other people’s inventory.

“It turns out that you don’t need to own Facebook, or LinkedIn, to sell their inventory and benefit monetarily.

“Yahoo switched from an owned and operated (O&O) destination to a network. It planned the majority of their revenues to come from off-property inventory.

“The belief, which I think makes a lot of sense, is that they could out-compete other players because they have better data.

“They had behavioural data. They knew when 43 million people were in the market for a car or wanted to buy tickets.

“If you aggregate that data and apply it across the broad reach of your network, you (can) out-compete other networks and promise a higher yield.

Yahoo’s display CPMs were cents even back then. This approach could only drag publishers down to unsustainably low CPMs, but down they went.

At Fairfax, I ran a project to identify the cost of producing a three-minute video. Correlated with the average number of views, the required breakeven CPM was $16.

No network paid that once it realised it could buy the audience cheaply through Google, and the video teams were fired.

Soon after, YouTube arrived offering a video player with ads built in. Any dollar is better than no dollar, they chuckled. Google owns YouTube.

A video ad on YouTube now sells for $70. Publishers get $8, and often less.

Rosenblatt’s not done.

“How do you execute that strategy, and get contracts to rep publishers? If you don't have access to that inventory, nothing else matters.

“The most efficient way is by owning the primary ad server that premium and non-premium publishers use to manage their inventory.”

We’re back to Gilgamesh and the siege. Rosenblatt explains:

“Nothing really matters but the platform. Nothing has such high switching costs. Switching is a nightmare. Takes an act of God to do it.”

That act of God phrase caught the attention of the Department of Justice and is a major plank of its antitrust case.

Rosenblatt wasn’t done:

“Let’s say DoubleClick and Google Ad Manager serve 18 billion impressions per day.

“Let’s say we’re able to peel off even 10 per cent of that inventory to monetise somehow. And I think the number should be higher.

“So that’s 1.8 billion impressions per day. If we monetise that at a dollar CPM and multiply that by 365, you get how valuable the platform is worth.”

Translation: If we can jazz hands publishers into giving us their inventory, and we syphon 10 per cent of the ad impressions off to our network, we make a motza.

Publishers not so much.

Rosenblatt continues.

“What happens to networks? Today there are a few hundred, Most people will say there are too many.

“There will be a shakeout, but two years from now, I think the opposite will happen.

“There will be thousands of pubs selling a small part of their inventory through small salesforces.

“Everything else will be dumped into two exchanges: The Google exchange, and probably the Yahoo exchange.

“Those two will end up controlling probably 90 per cent of display inventory.”

Google quickly beat Yahoo, and now has a 91 per cent share of the ad server market.

Rosenblatt adds:

“We’ll have created what’s comparable to the NYSE or the London Stock Exchange. In other words, we’ll do to display what Google did to search.”

The trials have heard Google has a 90 per cent of search, 95 per cent of mobile.

He continues:

“The whole business of being a network is knowing a little bit more about users.

“Let’s say you know who’s in the market for a surfboard. Today, if you're a surfboard manufacturer, it’s really hard to buy advertising.

“You either buy people searching for it, or you buy a small number of sites about surfboards.

“As a network, if you can figure out across the entire world who’s in the market for surfboards, you can aggregate.

“And then buy only those people out of these exchanges and resell them to the surfboard manufacturers.

“You can imagine networks buying at low price in the exchange and turning around and selling that back to the advertiser for a lot more.”

Google buys the premium publisher audience for peanuts, resells it for less peanuts through the exchange it owns, an advertiser buys it, pays Google to reach your audience…

Rosenblatt goes on:

“The audience is so fragmented, you need some mechanism to roll them up into one single large pool.

“It’s just not economical to do a thousand buys. For the same reason that in finance, there are many hedge funds who compete against Goldman Sachs.

“There are always going to be niches where it’s possible to know a lot about one specialty. It’s why there are vertical search engines, like travel sites. You know more about users; you can offer more. It’s depth v breadth.

“Mechanically, the way the surfboard network will do this is they go out and they do deals with all the different surfboard-related publishers, and they create cookie lists, and then buy those cookie lists out of the exchange. The networks' value is data.”

The process turns publishing’s premium lobster into Google’s data dogfood, which is fed via hyper-targeting to consumers.

A Googler asks what would incentivise publishers to provide more data to a rival network. Rosenblatt replies:

“You wouldn’t. Let’s look at YouTube. They use DFP. You’ve got your homepage units, and maybe some other very high value units elsewhere.

“That’s the stuff that our direct salesforce will sell. Everything else, you would dump into our exchange, and you let the entire world go to a single URL and bid.

“If you’re a purist about this, and more and more publishers are, you’d also let the market compete not just for the remnant stuff, but also for your premium inventory.

“…so if the market produces a higher bid than your sales force, it gets it. (It means) YouTube wins even if its sales force doesn’t.”

The antitrust trial has heard that Google execs were trained not to use anti-competitive terminology in their mails. Rosenblatt didn’t appear to get the memo.

He continued:

“Let’s switch gears to how we make sure we’ll out-compete everyone else.

“One way is by *not* putting all the same targeting technology we use for the GCN into the exchange.”

Think about that. Google knows your content, audience and data because you gave it to them. But they’re only going to use their best tech to monetise their own sites.

Rosenblatt used another phrase that caught the attention of the DoJ.

“We’re both Goldman and NYSE. If it turns out that another network is better, we still make money through the exchange.”

He’s talking about the 36 per cent fees Google charges everyone to use its tech. It means Google gets paid whether it wins or loses, and sees both sides of the market.

He continues:

“We also have better intelligence because we know how other networks are competing against us.

“It's the surfboard thing. If they aggregate data and build a customer database across all clients, they’ll be better able to know the value of a publisher’s inventory than the publisher.

“And they’ll do this in an automated way, with no IOs, fewer people involved, more efficient, get people in China to make the ads.

“The ultimate end state is there are very few people involved in the process. It’s automated.”

And that is how the publisher advertising model was demolished by a slidedeck, in Google’s own words.

So, here’s a picture of a kitten to make you feel better…

BTW, don’t get a kitten, get even. Tomorrow will bring another day of revelations at the historic antitrust case.

And PS: Remember the bankers.

Very good insight, as always 😊